First Quarter, 2024

Click here for a printable version of the Investment Update.

Chevy Chase Trust’s unique approach to Thematic Investing weaves together multiple themes across sectors, geographies, and industries, each designed to capitalize on research-driven insights. Listen to our quarterly update of economic conditions and investment strategy.

Everything we do starts with a conversation. Understanding your unique story is key in the development of a plan with your best interests in mind. To connect with us to learn more and begin a conversation, visit chevychasetrust.com.

To read the Q2 2024 Investment Update, visit https://www.chevychasetrust.com/second-quarter-2024/

For more information about Chevy Chase Trust, visit https://www.chevychasetrust.com/.

Important Disclosures This commentary is for informational purposes only. The information set forth herein is of a general nature and does not address the circumstances of any particular individual or entity. You should not construe any information herein as legal, tax, investment, financial or other advice. Nothing contained herein constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments. This commentary includes forward-looking statements, and actual results could differ materially from the views expressed. Materials referenced that were published by outside sources are included for informational purposes only. These sources contain facts and statistics quoted that appear to be reliable, but they may be incomplete or condensed and we do not guarantee their accuracy. Fact and circumstances may be materially different between the time of publication and the present time. Clients with different investment objectives, allocation targets, tax considerations, brokers, account sizes, historical basis in the applicable securities or other considerations will typically be subject to differing investment allocation decisions, including the timing of purchases and sales of specific securities, all of which cause clients to achieve different investment returns. Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment or investment strategy will be profitable, equal any historical performance level(s), be suitable for the portfolio or individual situation of any particular client, or otherwise prove successful. Investing involves risks, including the risk of loss of principal. The level of risk in a client’s portfolio will correspond to the risks of the underlying securities or other assets, which may decrease, sometimes rapidly or unpredictably, due to real or perceived adverse economic, political, or regulatory conditions, recessions, inflation, changes in interest or currency rates, lack of liquidity in the bond markets, the spread of infectious illness or other public health issues, armed conflict, trade disputes, sanctions or other government actions, or other general market conditions or factors. Actively managed portfolios are subject to management risk, which involves the chance that security selection or focus on securities in a particular style, market sector or group of companies will cause a portfolio to incur losses or underperform relative to benchmarks or other portfolios with similar investment objectives. Foreign investing involves special risks, including the potential for greater volatility and political, economic and currency risks. Please refer to Chevy Chase Trust’s Form ADV Part 2 Brochure, a copy of which is available upon request, for a more detailed description of the risks associated with Chevy Chase Trust’s investment strategy. The recipient assumes sole responsibility of evaluating the merits and risks associated with the use of any information herein before making any decisions based on such information.

Equity markets were strong globally in the first quarter. Easier financial conditions and expectations of both interest rate cuts and earnings growth drove strong performance. With the short-term outlook for rate cuts and other macroeconomic factors remaining fluid, we continue to manage risk and focus our research on our long-term investment themes.

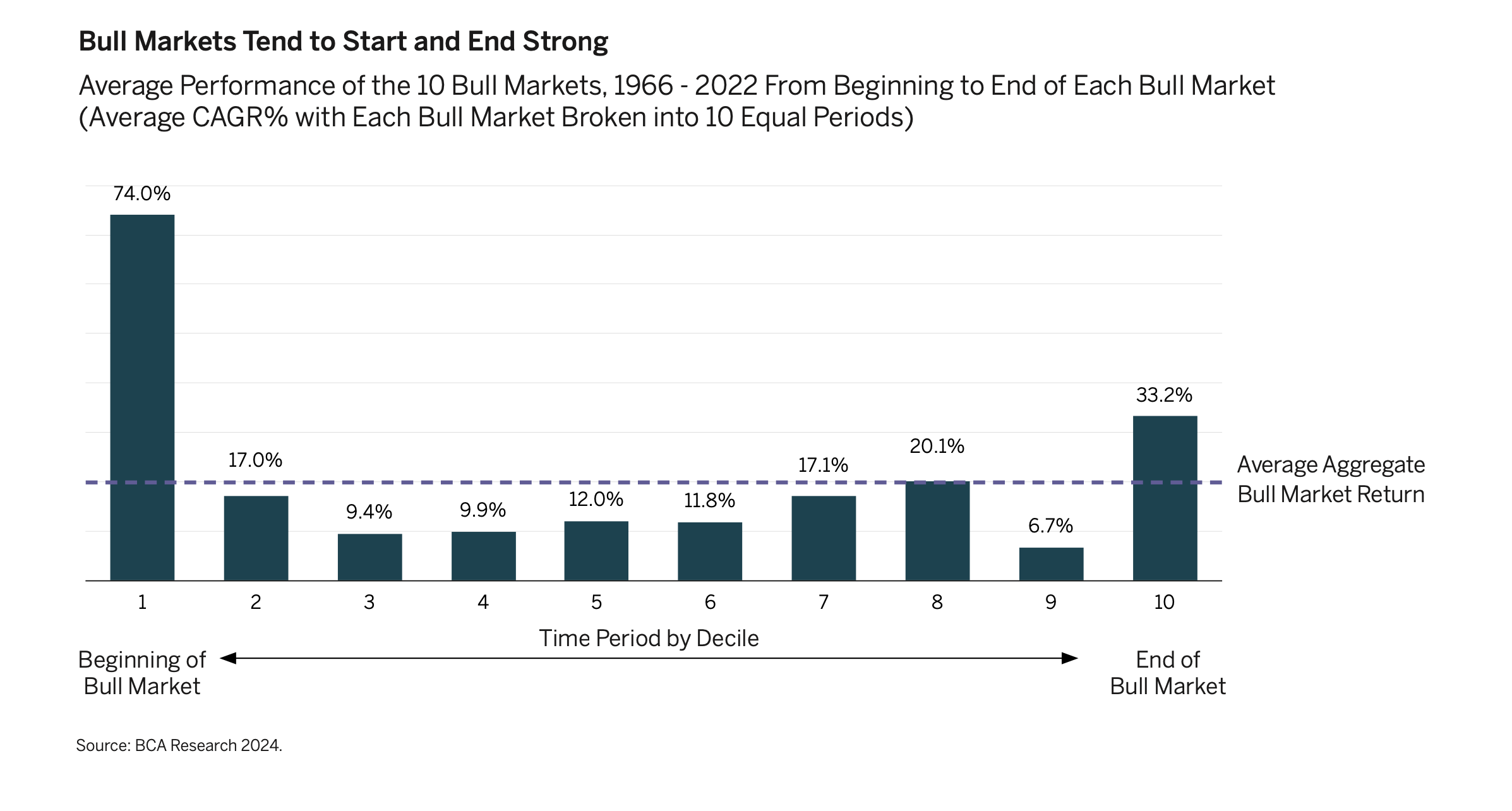

A Strong First Quarter

The S&P 500 reached all-time highs amid a global equity rally spurred by expectations of robust earnings, economic growth and central bank easing. The S&P 500 generated a total return of almost 11% for the quarter. It is now more than 50% higher than on October 1, 2022, and 23% higher than just six months ago. Meanwhile, Japan’s Nikkei Index soared over 20% in the first quarter and finally surpassed the bubble high it reached in 1989. Many other equity markets also reached all-time highs during the quarter, including France, Germany, India and Taiwan.

Underpinnings of the Global Rise In Equities

Several leading indicators suggest that global manufacturing growth is likely to pick up soon, and employment remains strong in most geographies. Throughout the developed world, unemployment is at its lowest level in more than 40 years, spurring capital investment consistent with our Next-Generation Automation theme. Coupled with lower inflation, rising employment typically leads to real wage growth, increased consumer demand and higher levels of business confidence. Any rebound in beleaguered China would further contribute to this improving situation.

Portfolio Positioning and Theme Updates

Given the dynamics discussed above, we have been prudent in managing risk in portfolios, trimming some positions and ensuring a high degree of diversification across sector, style and geography. In our Opportunities Abound Abroad theme, we have increased holdings in Japanese and European equities.

We believe that these are times when focusing on the long-term potential of our themes is particularly important. We are excited to share several recent developments in two of these.

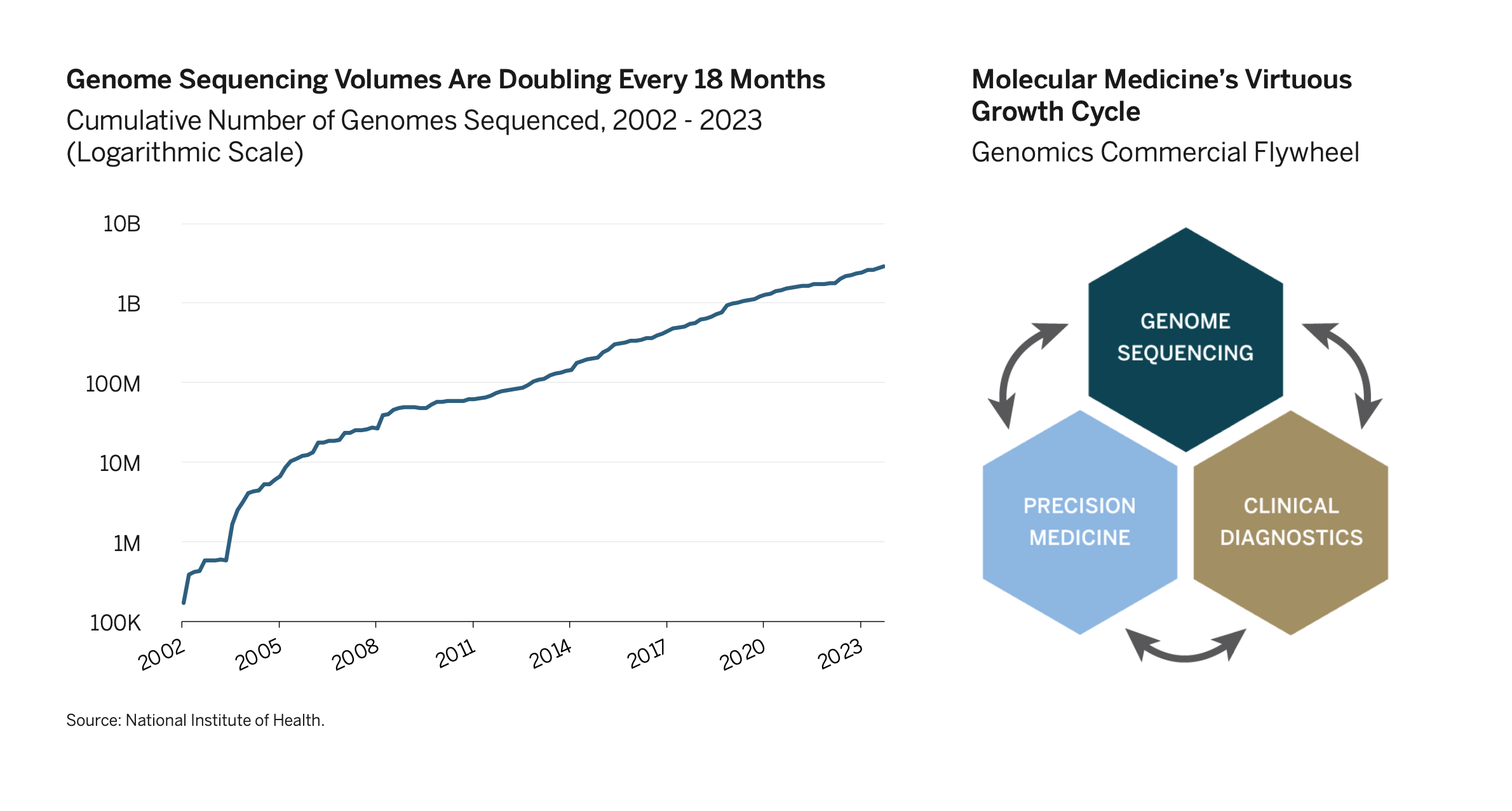

Advent of Molecular Medicine

While CKD was long understood to run in families, genomic sequencing has allowed diagnostic companies such as Natera to identify multiple genetic mutations that directly contribute to the development of kidney disease. This huge scientific breakthrough enabled biotech firms such as Vertex Pharmaceuticals to develop targeted medicines that could prevent or “fix” mutations and thus slow the progression of the disease. Without a treatment, patients would be unlikely to test for the mutation since the insight would not lead to an improvement in outcome. But diagnostic testing rates soar once information gained through the explosive growth in genomic sequencing leads to the development of new medicines.

Time will tell which specific companies will ultimately benefit from this virtuous cycle, but we have witnessed this pattern unfold for many diseases, and we expect it to repeat for many more. The sequencing of an increasing number of genomes leads to a better understanding of the root causes of disease, which leads to the development of targeted medicines. The development of targeted medicines, in turn, spurs increased diagnostic testing, which contributes to the scientific understanding of genetic linkages, encouraging even more advanced genomic sequencing. These mutually reinforcing trends create a flywheel that can power high rates of revenue and earnings growth across companies focused on diagnostics and treatment, as well as the technologies that enable them.

Important Disclosures This commentary is for informational purposes only. The information set forth herein is of a general nature and does not address the circumstances of any particular individual or entity. You should not construe any information herein as legal, tax, investment, financial or other advice. Nothing contained herein constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments. This commentary includes forward-looking statements, and actual results could differ materially from the views expressed. Materials referenced that were published by outside sources are included for informational purposes only. These sources contain facts and statistics quoted that appear to be reliable, but they may be incomplete or condensed and we do not guarantee their accuracy. Fact and circumstances may be materially different between the time of publication and the present time. Clients with different investment objectives, allocation targets, tax considerations, brokers, account sizes, historical basis in the applicable securities or other considerations will typically be subject to differing investment allocation decisions, including the timing of purchases and sales of specific securities, all of which cause clients to achieve different investment returns. Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment or investment strategy will be profitable, equal any historical performance level(s), be suitable for the portfolio or individual situation of any particular client, or otherwise prove successful. Investing involves risks, including the risk of loss of principal. The level of risk in a client’s portfolio will correspond to the risks of the underlying securities or other assets, which may decrease, sometimes rapidly or unpredictably, due to real or perceived adverse economic, political, or regulatory conditions, recessions, inflation, changes in interest or currency rates, lack of liquidity in the bond markets, the spread of infectious illness or other public health issues, armed conflict, trade disputes, sanctions or other government actions, or other general market conditions or factors. Actively managed portfolios are subject to management risk, which involves the chance that security selection or focus on securities in a particular style, market sector or group of companies will cause a portfolio to incur losses or underperform relative to benchmarks or other portfolios with similar investment objectives. Foreign investing involves special risks, including the potential for greater volatility and political, economic and currency risks. Please refer to Chevy Chase Trust’s Form ADV Part 2 Brochure, a copy of which is available upon request, for a more detailed description of the risks associated with Chevy Chase Trust’s investment strategy. The recipient assumes sole responsibility of evaluating the merits and risks associated with the use of any information herein before making any decisions based on such information.