Equity markets were strong globally in the first quarter. Easier financial conditions and expectations of both interest rate cuts and earnings growth drove strong performance. With the short-term outlook for rate cuts and other macroeconomic factors remaining fluid, we continue to manage risk and focus our research on our long-term investment themes.

A Strong First Quarter

The S&P 500 reached all-time highs amid a global equity rally spurred by expectations of robust earnings, economic growth and central bank easing. The S&P 500 generated a total return of almost 11% for the quarter. It is now more than 50% higher than on October 1, 2022, and 23% higher than just six months ago. Meanwhile, Japan’s Nikkei Index soared over 20% in the first quarter and finally surpassed the bubble high it reached in 1989. Many other equity markets also reached all-time highs during the quarter, including France, Germany, India and Taiwan.

Underpinnings of the Global Rise In Equities

The most recent rallies abroad reflect a combination of fundamental improvements in earnings and financial conditions. By contrast, the U.S. rally appears to be driven less by corporate results than by excitement over the potential of artificial intelligence and fears of missing out.

U.S. investors began to embrace the “soft-landing” narrative in mid 2023, when a widely expected recession did not materialize despite the largest rate hikes in 40 years. Then optimism soared in October 2023, when Federal Reserve Chairman Jerome Powell said he would be willing to lower interest rates before seeing clear signs of an economic contraction.

However, better-than-expected economic growth and falling inflation were not just U.S. phenomena. Inflation slowed almost everywhere as pandemic-related supply chain issues were eliminated. Several central banks – not just the Fed – have said they are likely to lower interest rates this year. As a result, global corporate spreads have narrowed considerably and bond yields have declined, boosting equity markets and economic activity globally.

Several leading indicators suggest that global manufacturing growth is likely to pick up soon, and employment remains strong in most geographies. Throughout the developed world, unemployment is at its lowest level in more than 40 years, spurring capital investment consistent with our Next-Generation Automation theme. Coupled with lower inflation, rising employment typically leads to real wage growth, increased consumer demand and higher levels of business confidence. Any rebound in beleaguered China would further contribute to this improving situation.

Portfolio Positioning and Theme Updates

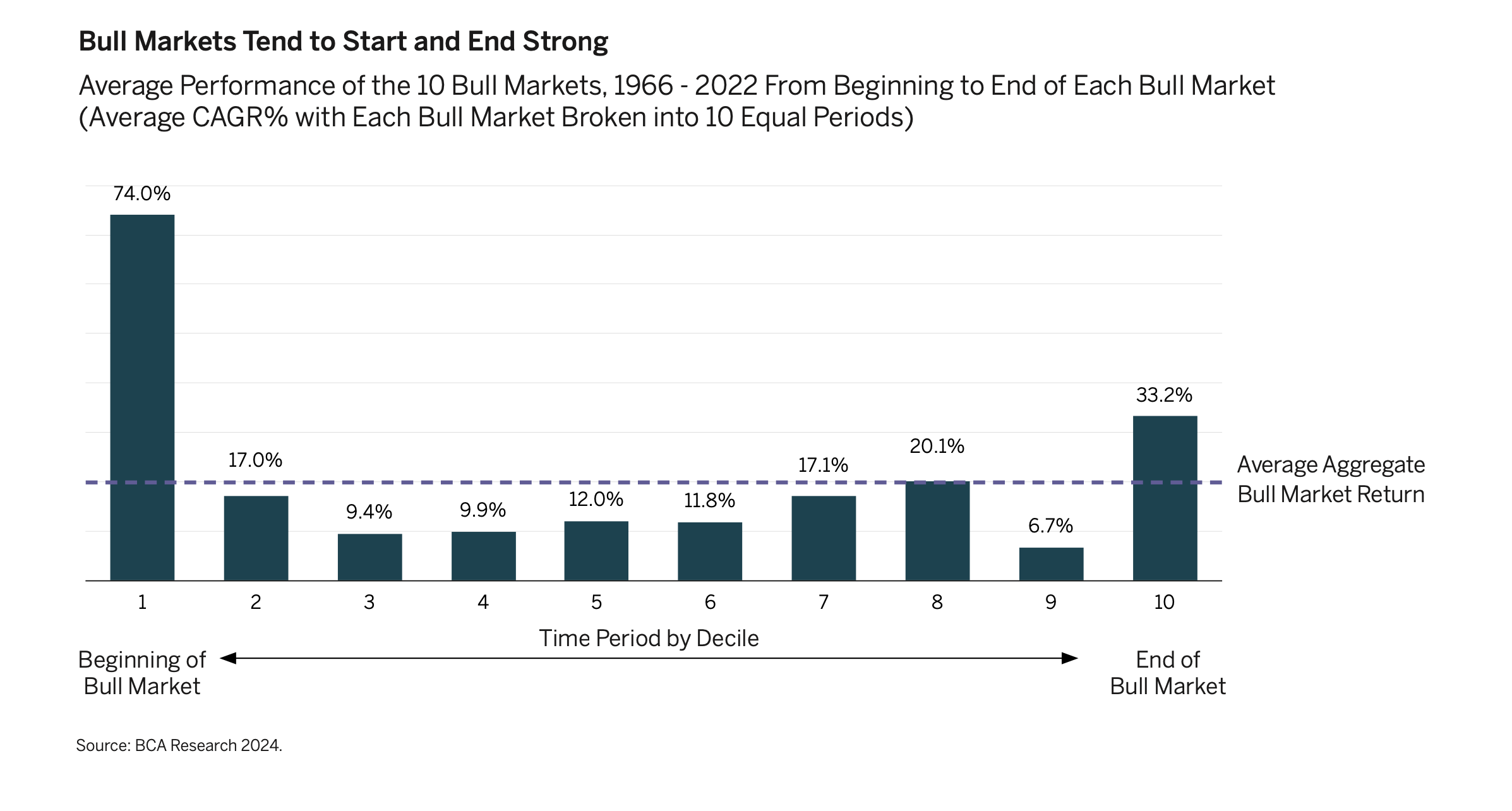

After the rally of the past six months, the S&P 500 looks quite expensive relative to both its own history and inflation-adjusted yields on long-term U.S. bonds. Currently the S&P 500 is trading at 21 times forward earnings estimates, significantly higher than its 2012 – 2019 average of 15.8. U.S. stock and bond markets now reflect very different economic outlooks. Equity investors appear to expect the strong earnings growth associated with a growing economy. Meanwhile the still-inverted yield curve shows bond investors are far more pessimistic.

High valuations don’t mean stocks won’t continue to rise in the months ahead, but we must acknowledge that markets cannot continue to increase at a double-digit quarterly rate indefinitely. The last stretch of a bull market tends to be very rewarding for those who remain invested, but it can also create a false sense of complacency that encourages investors to stay in too long. One of the most difficult challenges in investing is knowing when to take profits. Given the dynamics discussed above, we have been prudent in managing risk in portfolios, trimming some positions and ensuring a high degree of diversification across sector, style and geography. In our Opportunities Abound Abroad theme, we have increased holdings in Japanese and European equities. We believe that these are times when focusing on the long-term potential of our themes is particularly important. We are excited to share several recent developments in two of these.

Advent of Molecular Medicine

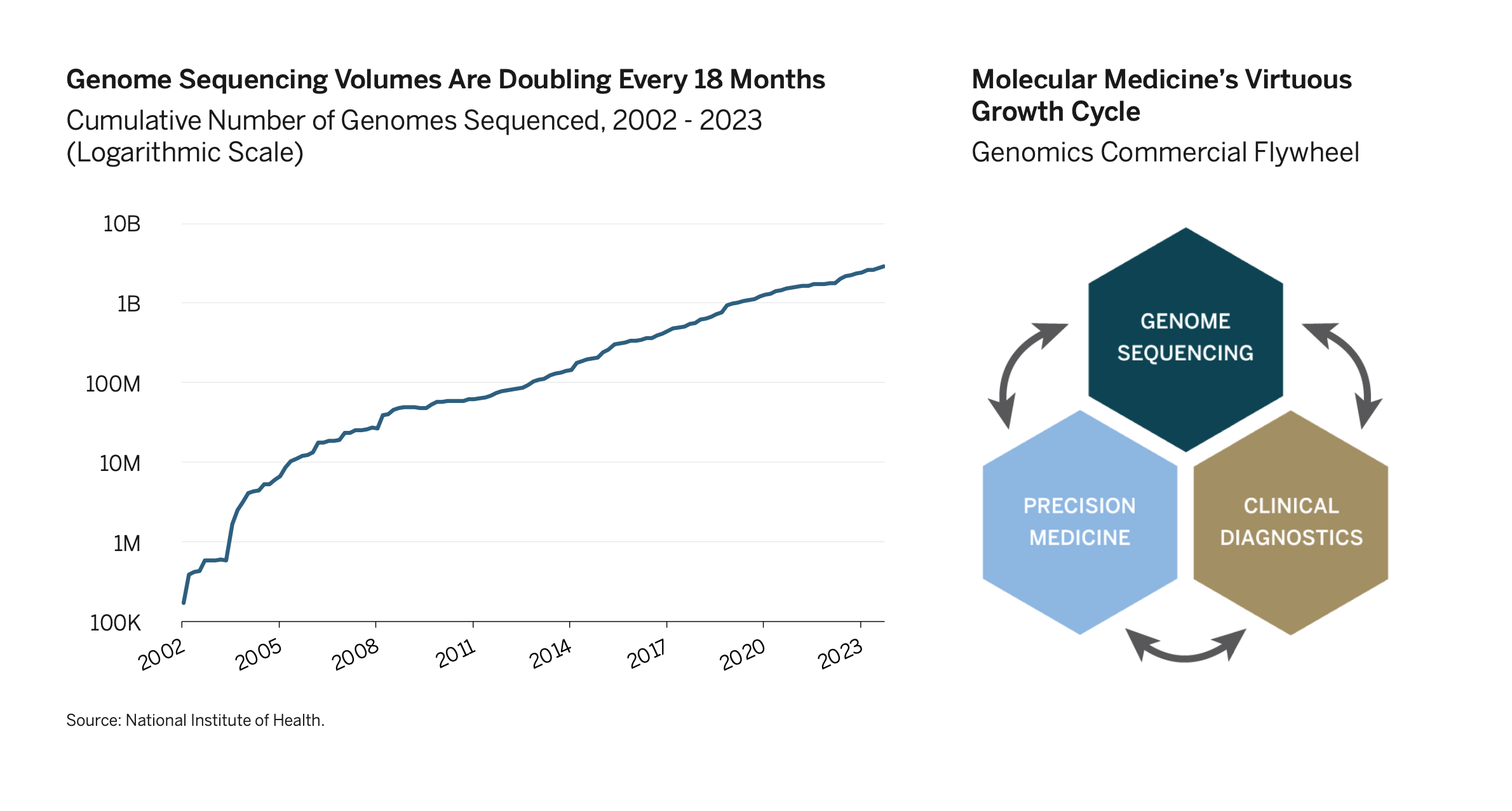

Our Molecular Medicine theme – one of our oldest – continues to unfold as we expected, with many positive and mutually reinforcing developments in this transformative science highlighting the growth potential of our investments. A good example of the power of molecular medicine and its virtuous growth cycle can be seen with respect to chronic kidney disease (CKD), which affects roughly one out of seven adults in the U.S. While CKD was long understood to run in families, genomic sequencing has allowed diagnostic companies such as Natera to identify multiple genetic mutations that directly contribute to the development of kidney disease. This huge scientific breakthrough enabled biotech firms such as Vertex Pharmaceuticals to develop targeted medicines that could prevent or “fix” mutations and thus slow the progression of the disease. Without a treatment, patients would be unlikely to test for the mutation since the insight would not lead to an improvement in outcome. But diagnostic testing rates soar once information gained through the explosive growth in genomic sequencing leads to the development of new medicines. Time will tell which specific companies will ultimately benefit from this virtuous cycle, but we have witnessed this pattern unfold for many diseases, and we expect it to repeat for many more. The sequencing of an increasing number of genomes leads to a better understanding of the root causes of disease, which leads to the development of targeted medicines. The development of targeted medicines, in turn, spurs increased diagnostic testing, which contributes to the scientific understanding of genetic linkages, encouraging even more advanced genomic sequencing. These mutually reinforcing trends create a flywheel that can power high rates of revenue and earnings growth across companies focused on diagnostics and treatment, as well as the technologies that enable them.

Post-Pandemic Consumer

Our consumer-related theme has evolved materially, as the COVID pandemic has ushered in work from home, potentially the biggest change to work arrangements since the Blackberry was introduced nearly 25 years ago. Working from home has had a profound impact on urban life and consumption patterns that we expect will endure. Thus, we have renamed our Converging Consumer theme the Post-Pandemic Consumer. Pre-pandemic, U.S. consumers increasingly preferred to live close to jobs in walkable central cities. But when the economic shutdown forced people to abandon their offices four years ago, many discovered they could work effectively from home and enjoyed the freedom it created. As the economy reopened, they sought to work from home at least a few days a week. Today, work from home in the U.S. has settled at about 30% of all workdays, down from its peak of 60%, but five times its pre-pandemic level. Work from home is also becoming more common abroad. While recent studies show that fully remote work reduces productivity by 10% on average, they also indicate that a hybrid approach (with roughly three days per week spent in the office) has little to no impact on productivity and can reduce costs. Workers prize the benefits of working from home so much that they are one-third less likely to quit jobs that permit it, reducing wage pressures. Lower wages and potential savings on space costs could increase profitability for companies with pragmatic hybrid work policies. Working from home has spurred many people to move away from city centers, particularly higher-income employees and younger workers. It has also led to people spending more time at or near home, and on travel and leisure activities. We are focusing our research in this theme on identifying the industries and companies most likely to benefit from these trends.

In Conclusion

We continue to navigate a complex and uncertain environment, with many crosscurrents. While we remain vigilant, we see promise on a variety of fronts.

In our fourth-quarter Investment Update, we discussed the massive outperformance of seven of the largest stocks relative to the rest of the S&P 500. While this persists, it has begun to moderate, with the valuations of some of these companies reflecting a more realistic view of their prospects. We are encouraged by the recent broadening of U.S. equity market performance. More than 85% of companies in the S&P 500 now trade above their 200-day moving average, compared to just 32% six months ago. It remains to be seen if these trends will usher in the reordering of market leadership that we have expected. We remain focused on our disciplined, long term–oriented and client-centered approach to investing. And as always, we are deeply grateful for our clients’ trust.

Important Disclosures This commentary is for informational purposes only. The information set forth herein is of a general nature and does not address the circumstances of any particular individual or entity. You should not construe any information herein as legal, tax, investment, financial or other advice. Nothing contained herein constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments. This commentary includes forward-looking statements, and actual results could differ materially from the views expressed. Materials referenced that were published by outside sources are included for informational purposes only. These sources contain facts and statistics quoted that appear to be reliable, but they may be incomplete or condensed and we do not guarantee their accuracy. Fact and circumstances may be materially different between the time of publication and the present time. Clients with different investment objectives, allocation targets, tax considerations, brokers, account sizes, historical basis in the applicable securities or other considerations will typically be subject to differing investment allocation decisions, including the timing of purchases and sales of specific securities, all of which cause clients to achieve different investment returns. Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment or investment strategy will be profitable, equal any historical performance level(s), be suitable for the portfolio or individual situation of any particular client, or otherwise prove successful. Investing involves risks, including the risk of loss of principal. The level of risk in a client’s portfolio will correspond to the risks of the underlying securities or other assets, which may decrease, sometimes rapidly or unpredictably, due to real or perceived adverse economic, political, or regulatory conditions, recessions, inflation, changes in interest or currency rates, lack of liquidity in the bond markets, the spread of infectious illness or other public health issues, armed conflict, trade disputes, sanctions or other government actions, or other general market conditions or factors. Actively managed portfolios are subject to management risk, which involves the chance that security selection or focus on securities in a particular style, market sector or group of companies will cause a portfolio to incur losses or underperform relative to benchmarks or other portfolios with similar investment objectives. Foreign investing involves special risks, including the potential for greater volatility and political, economic and currency risks. Please refer to Chevy Chase Trust’s Form ADV Part 2 Brochure, a copy of which is available upon request, for a more detailed description of the risks associated with Chevy Chase Trust’s investment strategy. The recipient assumes sole responsibility of evaluating the merits and risks associated with the use of any information herein before making any decisions based on such information.

7501 Wisconsin Avenue, Suite 1500W

Bethesda, Maryland 20814

240.497.5000

8201 Greensboro Drive, Suite 450

McLean, Virginia 22102

Given the dynamics discussed above, we have been prudent in managing risk in portfolios, trimming some positions and ensuring a high degree of diversification across sector, style and geography. In our Opportunities Abound Abroad theme, we have increased holdings in Japanese and European equities. We believe that these are times when focusing on the long-term potential of our themes is particularly important. We are excited to share several recent developments in two of these.

Given the dynamics discussed above, we have been prudent in managing risk in portfolios, trimming some positions and ensuring a high degree of diversification across sector, style and geography. In our Opportunities Abound Abroad theme, we have increased holdings in Japanese and European equities. We believe that these are times when focusing on the long-term potential of our themes is particularly important. We are excited to share several recent developments in two of these. Time will tell which specific companies will ultimately benefit from this virtuous cycle, but we have witnessed this pattern unfold for many diseases, and we expect it to repeat for many more. The sequencing of an increasing number of genomes leads to a better understanding of the root causes of disease, which leads to the development of targeted medicines. The development of targeted medicines, in turn, spurs increased diagnostic testing, which contributes to the scientific understanding of genetic linkages, encouraging even more advanced genomic sequencing. These mutually reinforcing trends create a flywheel that can power high rates of revenue and earnings growth across companies focused on diagnostics and treatment, as well as the technologies that enable them.

Time will tell which specific companies will ultimately benefit from this virtuous cycle, but we have witnessed this pattern unfold for many diseases, and we expect it to repeat for many more. The sequencing of an increasing number of genomes leads to a better understanding of the root causes of disease, which leads to the development of targeted medicines. The development of targeted medicines, in turn, spurs increased diagnostic testing, which contributes to the scientific understanding of genetic linkages, encouraging even more advanced genomic sequencing. These mutually reinforcing trends create a flywheel that can power high rates of revenue and earnings growth across companies focused on diagnostics and treatment, as well as the technologies that enable them.