Fourth Quarter, 2023

Click here for a printable version of the Investment Update.

Click here to listen to an audio version of the Investment Update.

Chevy Chase Trust’s unique approach to Thematic Investing weaves together multiple themes across sectors, geographies, and industries, each designed to capitalize on research-driven insights. Listen to our quarterly update of economic conditions and investment strategy.

Everything we do starts with a conversation. Understanding your unique story is key in the development of a plan with your best interests in mind. To connect with us to learn more and begin a conversation, visit chevychasetrust.com.

To read the Q3 2024 Investment Update, visit https://www.chevychasetrust.com/third-quarter-2024/. For more information about Chevy Chase Trust, visit https://www.chevychasetrust.com/.

Important Disclosures This commentary is for informational purposes only. The information set forth herein is of a general nature and does not address the circumstances of any particular individual or entity. You should not construe any information herein as legal, tax, investment, financial or other advice. Nothing contained herein constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments. This commentary includes forward-looking statements, and actual results could differ materially from the views expressed. Materials referenced that were published by outside sources are included for informational purposes only. These sources contain facts and statistics quoted that appear to be reliable, but they may be incomplete or condensed and we do not guarantee their accuracy. Fact and circumstances may be materially different between the time of publication and the present time. Clients with different investment objectives, allocation targets, tax considerations, brokers, account sizes, historical basis in the applicable securities or other considerations will typically be subject to differing investment allocation decisions, including the timing of purchases and sales of specific securities, all of which cause clients to achieve different investment returns. Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment or investment strategy will be profitable, equal any historical performance level(s), be suitable for the portfolio or individual situation of any particular client, or otherwise prove successful. Investing involves risks, including the risk of loss of principal. The level of risk in a client’s portfolio will correspond to the risks of the underlying securities or other assets, which may decrease, sometimes rapidly or unpredictably, due to real or perceived adverse economic, political, or regulatory conditions, recessions, inflation, changes in interest or currency rates, lack of liquidity in the bond markets, the spread of infectious illness or other public health issues, armed conflict, trade disputes, sanctions or other government actions, or other general market conditions or factors. Actively managed portfolios are subject to management risk, which involves the chance that security selection or focus on securities in a particular style, market sector or group of companies will cause a portfolio to incur losses or underperform relative to benchmarks or other portfolios with similar investment objectives. Foreign investing involves special risks, including the potential for greater volatility and political, economic and currency risks. Please refer to Chevy Chase Trust’s Form ADV Part 2 Brochure, a copy of which is available upon request, for a more detailed description of the risks associated with Chevy Chase Trust’s investment strategy. The recipient assumes sole responsibility of evaluating the merits and risks associated with the use of any information herein before making any decisions based on such information.

Strong equity market performance in 2023 has many investors entering 2024 optimistic about the economy and markets. While we see risks in the broader market, we also see neglected investment opportunities at home and abroad.

A Year That Defied Expectations

▪ The aging population and widespread deleveraging made consumers and businesses less sensitive to rising interest rates.

▪ The economy was simply returning to normal after the convulsions of the pandemic (see sidebar).

▪ It takes time for rate hikes to slow the economy, and we have yet to see their full impact.

All four of these explanations may be true to some degree. We see a path for the soft-landing investors have now come to expect, but this is not our base case. We think the most aggressive monetary policy tightening in 40 years is likely to slow the economy. While this has not happened yet, consumer spending is slowing, often a signal of a broader slowdown ahead.

Looking Ahead

We see several potential negative surprises that could trip up the market in 2024. Most notably:

▪ Lackluster results from the so-called Magnificent Seven could lead to a repricing of these mega-cap stocks.

Profit Margins

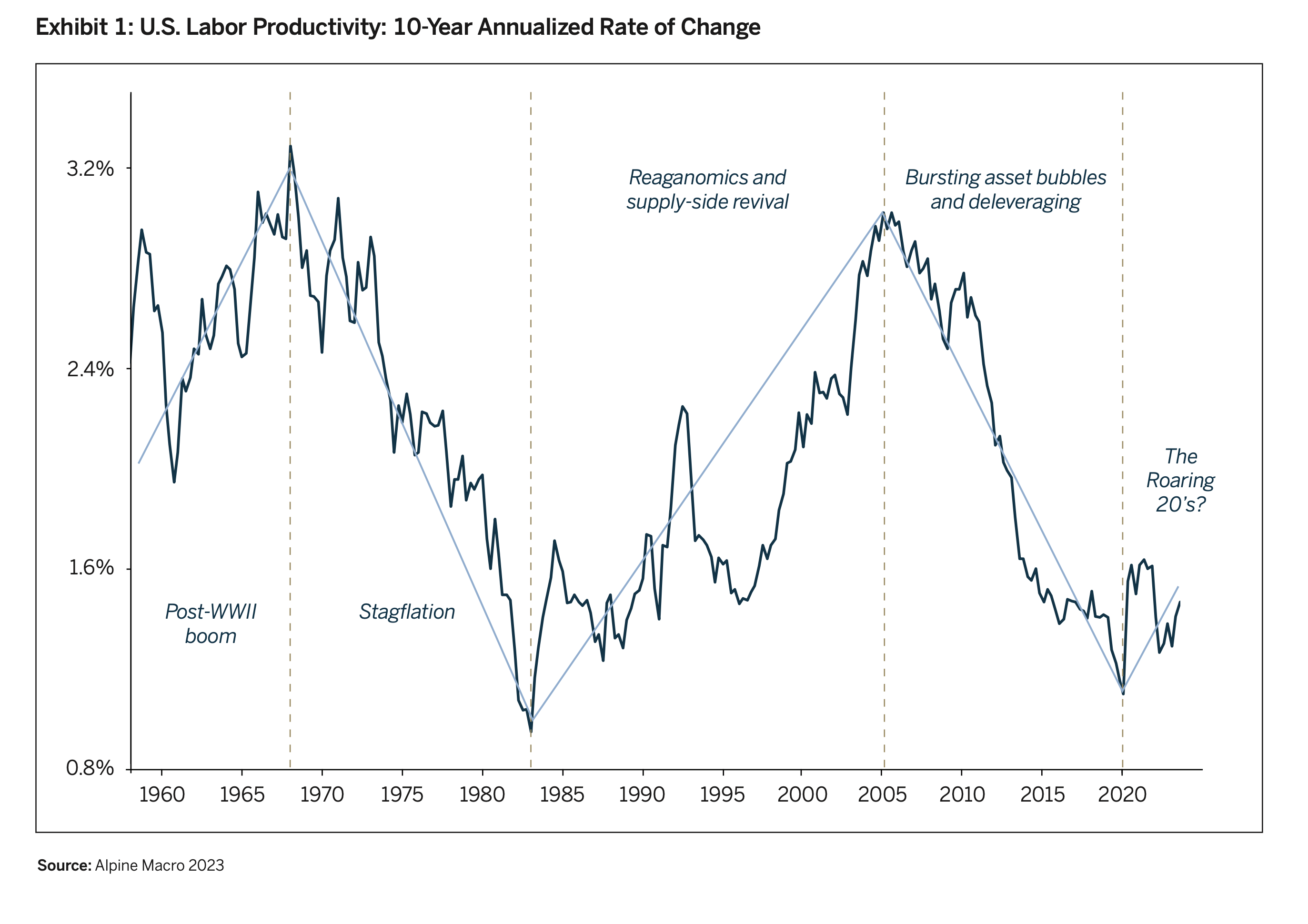

Some bulls attribute the recent strong growth in profit margins to improving labor productivity, which goes through long waves, with wars or major crises often acting as inflection points (Exhibit 1). Optimists suggest the 2020 pandemic was the much-needed catalyst to push the U.S. economy out of a long decline in productivity and income growth. It’s possible. For example, there has been a five-fold increase in working from home since the pandemic began. Recent research has found that working three days a week in the office and two at home does not reduce productivity and allows firms to save on recruitment and employee retention costs.

The Magnificent Seven

There’s another reason we are skeptical of continued broad strength in profit margins and returns. Both depend on continued strength for the S&P 500’s seven largest companies by market capitalization: Apple, Microsoft, Amazon, Nvidia, Alphabet (Google), Meta (Facebook) and Tesla. Together, these stocks delivered over 60% of the Index’s return in 2023— and each of them gained more than $300 billion in market capitalization, more than the total market cap of all but 20 names in the Index.

For the past decade, superior products and business strategies have driven rapid sales and earnings growth for the Magnificent Seven. But the most recent data suggest that sales growth for these companies is now running no faster than nominal GDP growth. In addition, government pressures in Europe and the U.S. are beginning to erode their monopolistic positions and pricing power.

This is concerning. Expectations of continued rapid sales and earnings growth—and fear of betting against a juggernaut— have led almost every class of investor to have significant exposure to these companies. As a result, each appears to be somewhere between fully priced and extremely expensive. Given their outsize weight in the S&P 500, disappointing results for these widely-held and richly-valued stocks could drive a decline in the Index.

Important Disclosures This commentary is for informational purposes only. The information set forth herein is of a general nature and does not address the circumstances of any particular individual or entity. You should not construe any information herein as legal, tax, investment, financial or other advice. Nothing contained herein constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments. This commentary includes forward-looking statements, and actual results could differ materially from the views expressed. Materials referenced that were published by outside sources are included for informational purposes only. These sources contain facts and statistics quoted that appear to be reliable, but they may be incomplete or condensed and we do not guarantee their accuracy. Fact and circumstances may be materially different between the time of publication and the present time. Clients with different investment objectives, allocation targets, tax considerations, brokers, account sizes, historical basis in the applicable securities or other considerations will typically be subject to differing investment allocation decisions, including the timing of purchases and sales of specific securities, all of which cause clients to achieve different investment returns. Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment or investment strategy will be profitable, equal any historical performance level(s), be suitable for the portfolio or individual situation of any particular client, or otherwise prove successful. Investing involves risks, including the risk of loss of principal. The level of risk in a client’s portfolio will correspond to the risks of the underlying securities or other assets, which may decrease, sometimes rapidly or unpredictably, due to real or perceived adverse economic, political, or regulatory conditions, recessions, inflation, changes in interest or currency rates, lack of liquidity in the bond markets, the spread of infectious illness or other public health issues, armed conflict, trade disputes, sanctions or other government actions, or other general market conditions or factors. Actively managed portfolios are subject to management risk, which involves the chance that security selection or focus on securities in a particular style, market sector or group of companies will cause a portfolio to incur losses or underperform relative to benchmarks or other portfolios with a similar investment objectives. Foreign investing involves special risks, including the potential for greater volatility and political, economic and currency risks. Please refer to Chevy Chase Trust’s Form ADV Part 2 Brochure, a copy of which is available upon request, for a more detailed description of the risks associated with Chevy Chase Trust’s investment strategy. The recipient assumes sole responsibility of evaluating the merits and risks associated with the use of any information herein before making any decisions based on such information.