Fourth Quarter, 2022

Click here for a printable version of the Investment Update.

January 9, 2023 – During 2022 the financial markets faced an extraordinary confluence of challenging events. Inflation hit its highest level in four decades. Interest rates rose at an unprecedented pace. War broke out in Europe. And China continued to impose pandemic-related lockdowns that hobbled its economy.

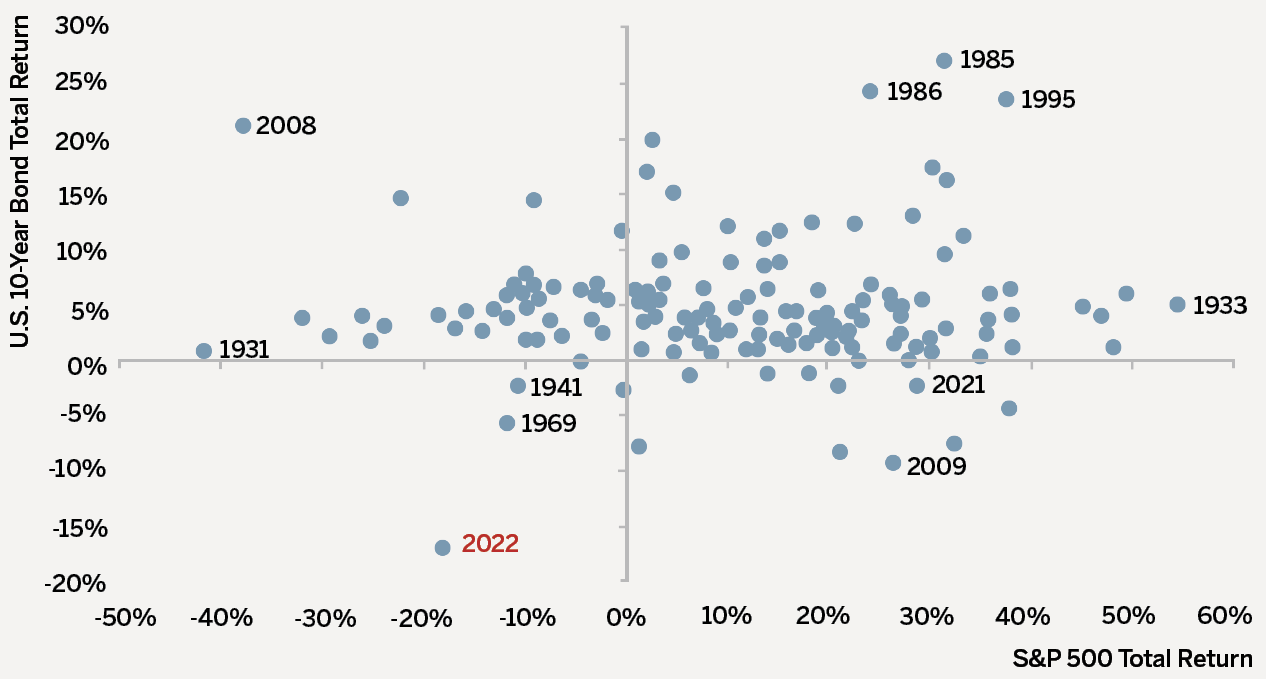

Against this backdrop, U.S. equities and bonds were both down sharply, making 2022 among the worst years for investors in a century (Exhibit 1). During 2022 the S&P 500 generated a loss of 18.1%, and the Bloomberg Aggregate bond index lost 13.0%.

Exhibit 1: U.S. Equity and 10-Year Bond Annual Total Returns (1872-2022)

Source: CLSA, Refinitiv, Robert Shiller – Yale University, Department of Economics

While market performance in 2022 was disappointing, it is important to view it in context. Over the prior three years, the S&P 500 rose over 90%, and with dividends, returned over 100%, while the Bloomberg Aggregate returned 15%. In 2022 the equity index gave up a small portion of its gains from 2019 through 2021, and the bond index settled back to its level at the beginning of 2019.

Inflation at the Root of It All

The 2022 decline in the financial markets was driven in large part by the U.S. Federal Reserve’s rapid about-face on inflation. At the start of the year, the Fed saw inflation as “transitory,” and thought that only a modest interest rate increase was needed to tame it. At the end of 2021, a majority of Fed Governors expected the Fed Funds Rate to end 2022 at only 0.9%. Just a few months later, persistent high inflation led the Fed to completely change its position and embark on a series of large rate hikes. By the end of 2022, the Fed Funds Rate had climbed to 4.25%-4.50%, and 17 of the 19 Fed Governors expected it to rise above 5.00% in the first half of 2023.

At Chevy Chase Trust, we began to think differently about inflation earlier than many. In mid-2020, as the Federal government distributed massive pandemic-related stimulus, we recognized that the low-inflation paradigm of the prior two decades was ending.

To properly assess inflation’s likely evolution, we developed a new inflation framework that explicitly separated the shorter-term, cyclical drivers of inflation on which most of the market focuses, from the longer-term, secular drivers of inflation that we believe will have a more profound impact over time. This work led us to add the End of Disinflationary Tailwinds theme to our Thematic Equity portfolios a few months later.

We first published our inflation matrices in our Investment Update — July 2021, and we have continued to refine our analysis since then.

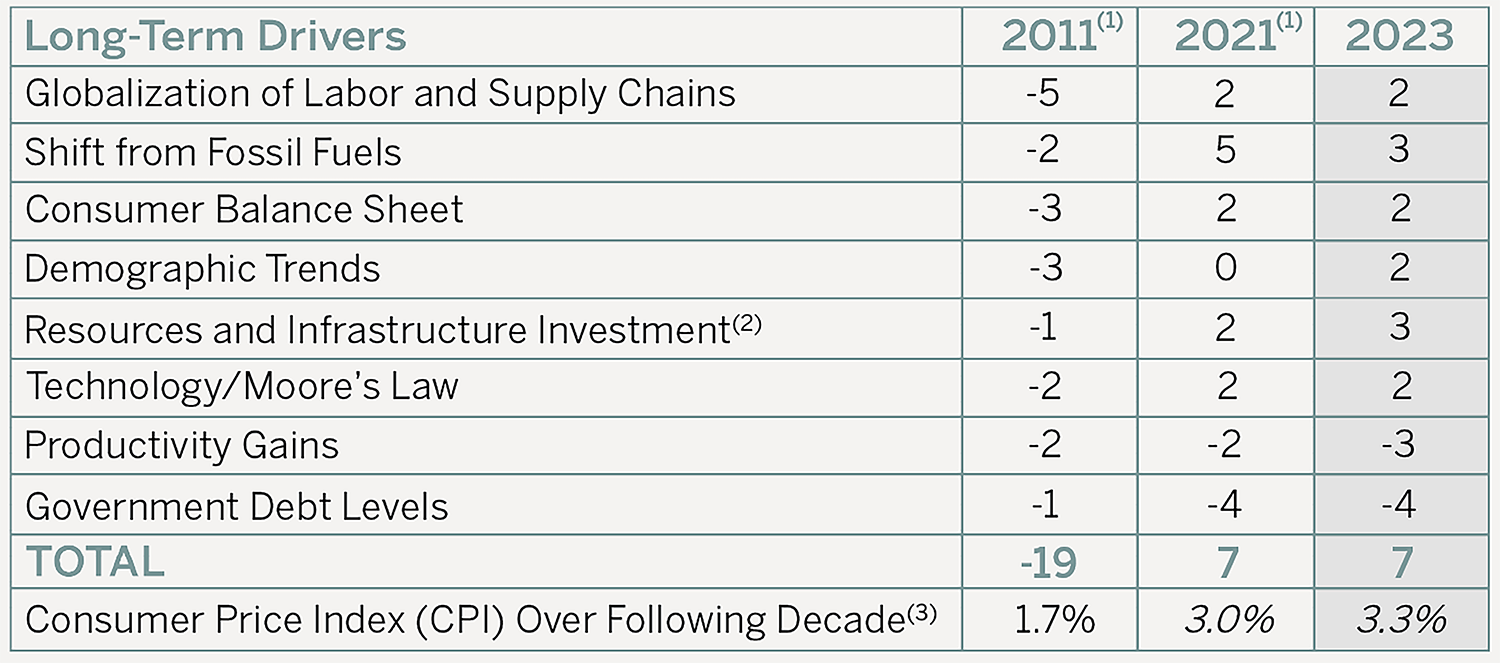

Our view on long-term, secular inflation remains largely unchanged (Exhibit 2).

Exhibit 2: Chevy Chase Trust Long-Term Inflation Matrix

(1) 2011 and 2021 calculated as of end of Q2 2021.

(2) Driver added in May 2022.

(3) 2011-2022 average annual CPI, and Chevy Chase Trust forecasts for average annual CPI for 2021-2031 and 2023-2033.

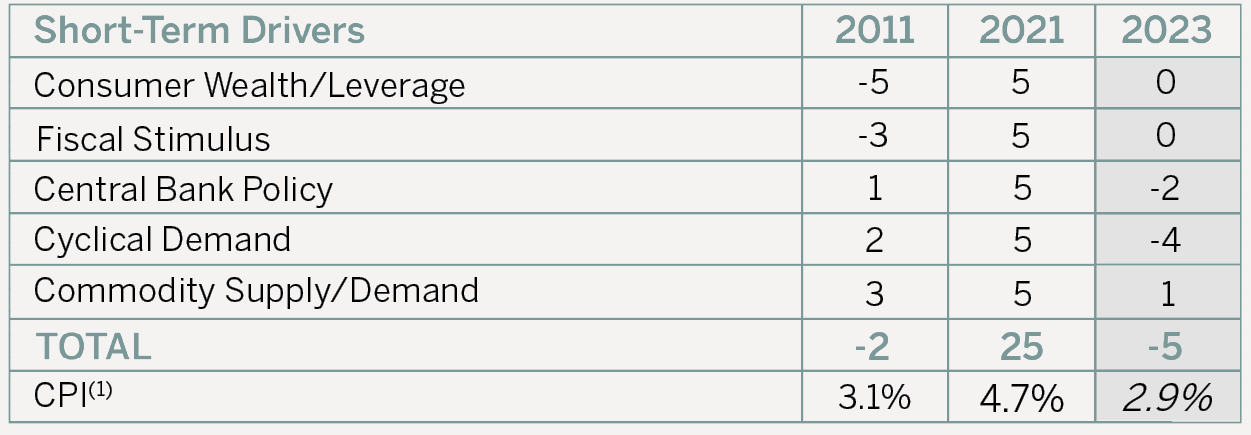

However, our short-term inflation matrix has changed dramatically (Exhibit 3).

Exhibit 3: Chevy Chase Trust Short-Term Inflation Matrix

(1) CPI data are average for 2011 and 2021 and Chevy Chase Trust projection for 2023.

We expect inflation to fall sharply over the next six to nine months, which should benefit both stocks and bonds. While we believe the Fed will remain hawkish to keep long-term inflation expectations anchored, inflation has already started to come down, and we expect its decline will continue. We wouldn’t be surprised to see inflation fall below the Fed’s current 2% target in the second half of 2023, before eventually moving up to the rates suggested by our long-term matrix.

A Mild Recession Probably Lies Ahead

Economic concerns are shifting from inflation to recession because the Fed has raised interest rates so much that the current inflationary fire is running out of fuel. Classic indicators all suggest that an economic slowdown lies ahead for the developed world. But our sense is that consumers flush with cash will delay its onset, and a broadly sound private sector will muffle its severity. Neither households nor businesses are over-extended, and regulation has converted banks from accelerants of recession to firebreaks.

Four factors should delay the onset and reduce the severity of a U.S. recession.

-

- Job openings remain elevated across all industry groups. In November, there were 1.7 job openings per unemployed worker, nearly 50% higher than in December 2019. Most workers who lose their jobs should have little difficulty finding new ones. The ongoing scarcity of labor suggests businesses may be reluctant to shed as many jobs in a recession as they might have otherwise. Joblessness is unlikely to rise sharply.

- Adjusted for inflation, disposable personal income rebounded in the third quarter of 2022, after declining for five quarters. We expect the uptrend to continue into 2023, because inflation-adjusted wages rarely decline when unemployment is low. As inflation falls, real wage growth will likely turn positive, even if nominal wage growth slows.

- Although U.S. households have spent much of their stimulus payments, consumers still have roughly $1.5 trillion more in savings than they did before the pandemic, the equivalent of 5.8% of U.S. annual GDP.

- While business surveys about expected capital investment point to some softness ahead, the decline is unlikely to be dramatic. Capital spending is already very low compared to historical norms, and the average age of nonresidential capital stock is higher than at any point in almost 60 years. We also expect businesses to increase capital investment to address the longer-term labor shortage that many large economies face.

Portfolio Positioning

Our portfolios have migrated to reflect our current outlook: near-term declines in inflation, a delayed and mild recession, followed by inflation and interest rates that will be higher than those seen during the past two decades. We expect bonds to be less correlated with equities than they were in 2022. This should provide more diversification benefit if a recession proves deeper than we expect.

In our Thematic Equity portfolios, we have trimmed positions in our End of Disinflationary Tailwinds theme, which performed well in 2022. Although we still like their longer-term prospects, we think these stocks may underperform in the short-term as inflation declines. We used the proceeds of these sales to add to positions in both our Dawn of Heterogenous Computing and Next-Generation Automation and Supply Chain Transformation themes. Many of our positions in these two themes fell considerably in 2022, partially reversing gains from prior years. We believe current prices represent an attractive entry point for these companies, which are also likely to rise if inflation declines early in the year, as we expect.

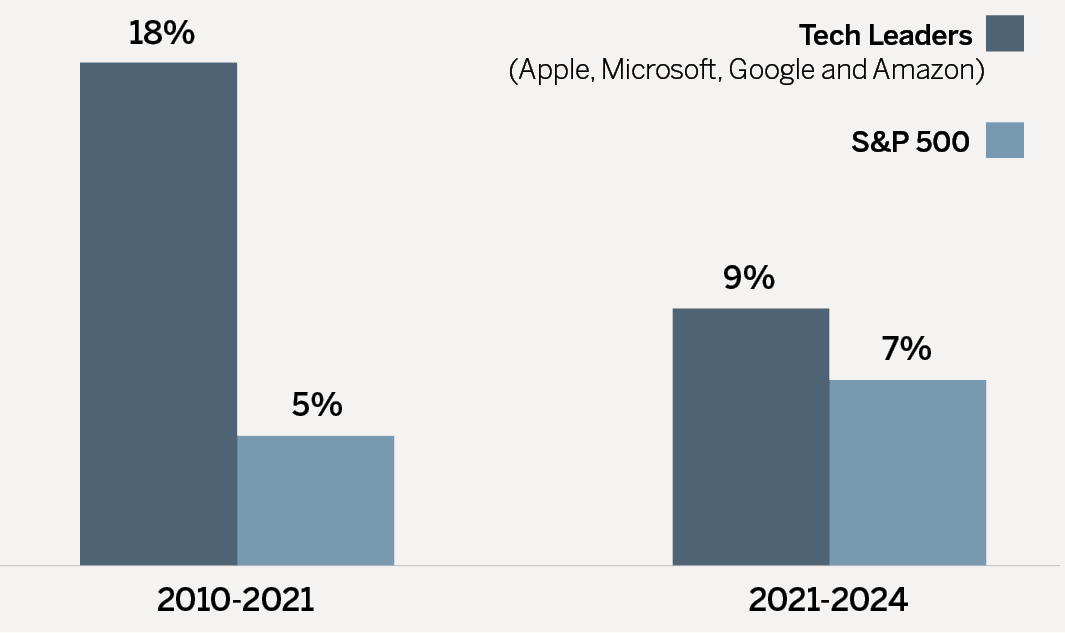

We also continued to trim our positions in the largest Growth stocks, including Apple, Microsoft, Google and Amazon. Despite stock price drops in 2022 that ranged from 26% to 49%, we believe these companies are still viewed too optimistically. Our research suggests that during the pandemic, each of these companies had gains in sales and earnings that would otherwise have taken several more years to achieve. In comparison to those massive gains, near-term results may look mediocre, at best (Exhibit 4).

Exhibit 4: Past and Estimated Future Sales Growth of Tech Leaders vs. S&P 500

Compound Annual Growth Rate

Source: Goldman Sachs Global Investment Research, FactSet

Market leadership often shifts in bear markets. We believe that once a bear market starts, investors should focus on identifying the next winning trend, rather than trying to time a reentry into the prior bull market trends that may now be defunct. We believe many of our current themes are well-positioned for this new era of market leadership, given the powerful secular changes they exploit. We are particularly optimistic about opportunities in our Next-Generation Automation and Supply Chain Transformation, Advent of Molecular Medicine, and End of Disinflationary Tailwinds themes.

We have also begun to increase positions in non-U.S. markets, particularly European stocks, which remain at a historic discount to U.S. equities, reflecting what we deem to be undue pessimism about the outlook for Europe (see box).

We enter the New Year with ample – though guarded – optimism in the markets, where being nimble and discerning may be more important than ever. We believe this flexibility, paired with confidence in our Thematic approach will serve us well. Thank you for your continued trust.

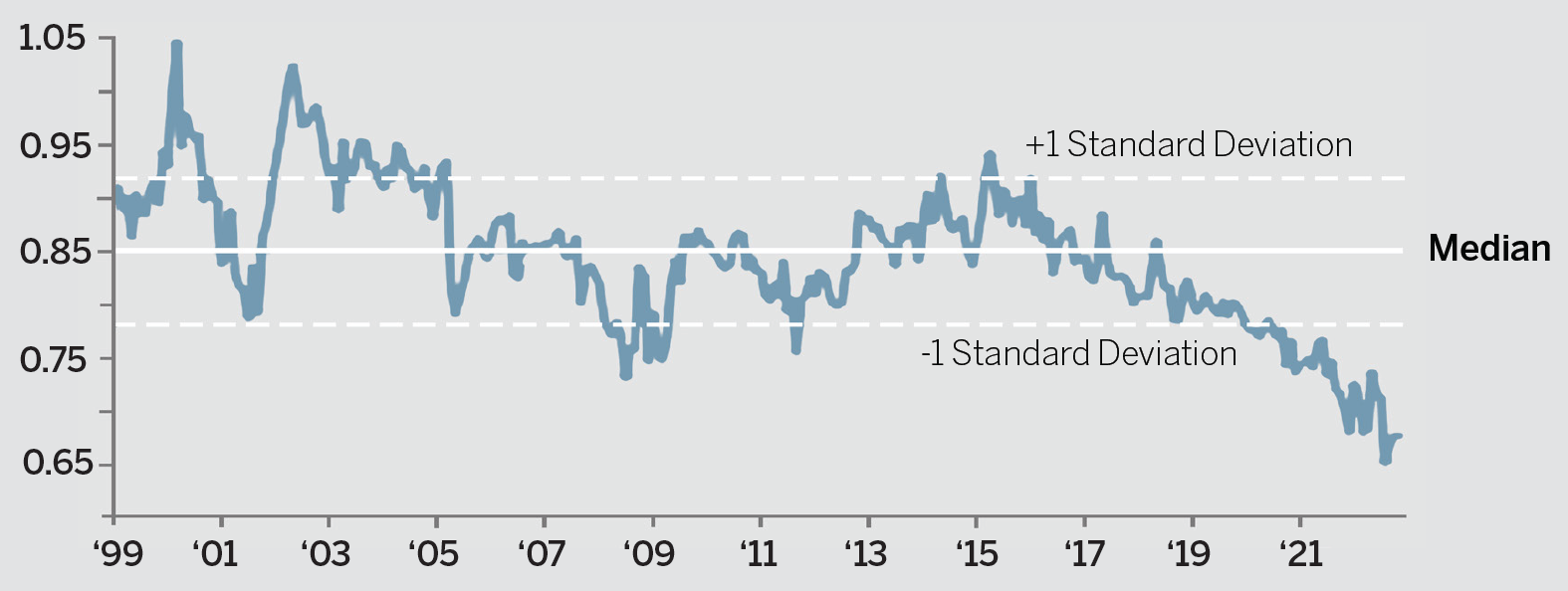

Opportunity Knocks in EuropeEurope is less far along than the U.S. in its recovery from the pandemic. Wage growth there has been lackluster, and durable goods spending remains well below its pre-pandemic trend. Furthermore, European inflation largely stems from disruptions to energy supplies related to the war in Ukraine. Core inflation in Europe is far lower than in the U.S. We think Europe’s outlook is better than it may seem. While energy supplies in Europe remain constrained, policymakers in the region reacted with uncharacteristic haste to replace Russia as their source of gas supplies. Germany completed the construction of its first floating liquid natural gas terminal in late 2022 and aims to have five floating units operating by the end of 2023. New pipelines are also being constructed. Last Fall, gas started flowing from Norway to Poland. In the meantime, efforts to conserve gas are proving less onerous than previously feared. In a recent ifo Institute survey, 75% of German companies reported that they were able to curb gas usage without cutting production. Defying expectations of a big decline, euro-area industrial production remained resilient in 2022. European households have accumulated savings that can support spending until the energy shock subsides, and credit growth remains above pre-pandemic levels. Europe doesn’t have to grow faster than the U.S. for European stocks to outperform. With valuations so depressed, just beating low expectations could power a strong rebound (Exhibit 5). We’re looking for attractive opportunities in Europe, particularly in Industrial, Energy and Consumer Discretionary stocks that are well positioned to capitalize on a European recovery; are well-aligned to our Increasing Wealth Concentration, Long- Term Covid Beneficiaries and End of Disinflationary Tailwinds themes; and trade at a discount to their U.S. peers. Exhibit 5: European vs. U.S. Forward Equity Price-to-Earnings Multiples (1999-2022)

Source: IBES, Datastream, Barclays Research |