First Quarter, 2023

Click here for a printable version of the Investment Update.

April 5, 2023 – The first quarter was a tumultuous start to the year. In the space of just three months, we saw:

- A strong January for equity markets after a challenging 2022

- A February pullback driven by higher-than-expected inflation and fears of higher interest rates

- A crisis in U.S. regional banks and a subsequent decline in yields that once again buoyed equity markets

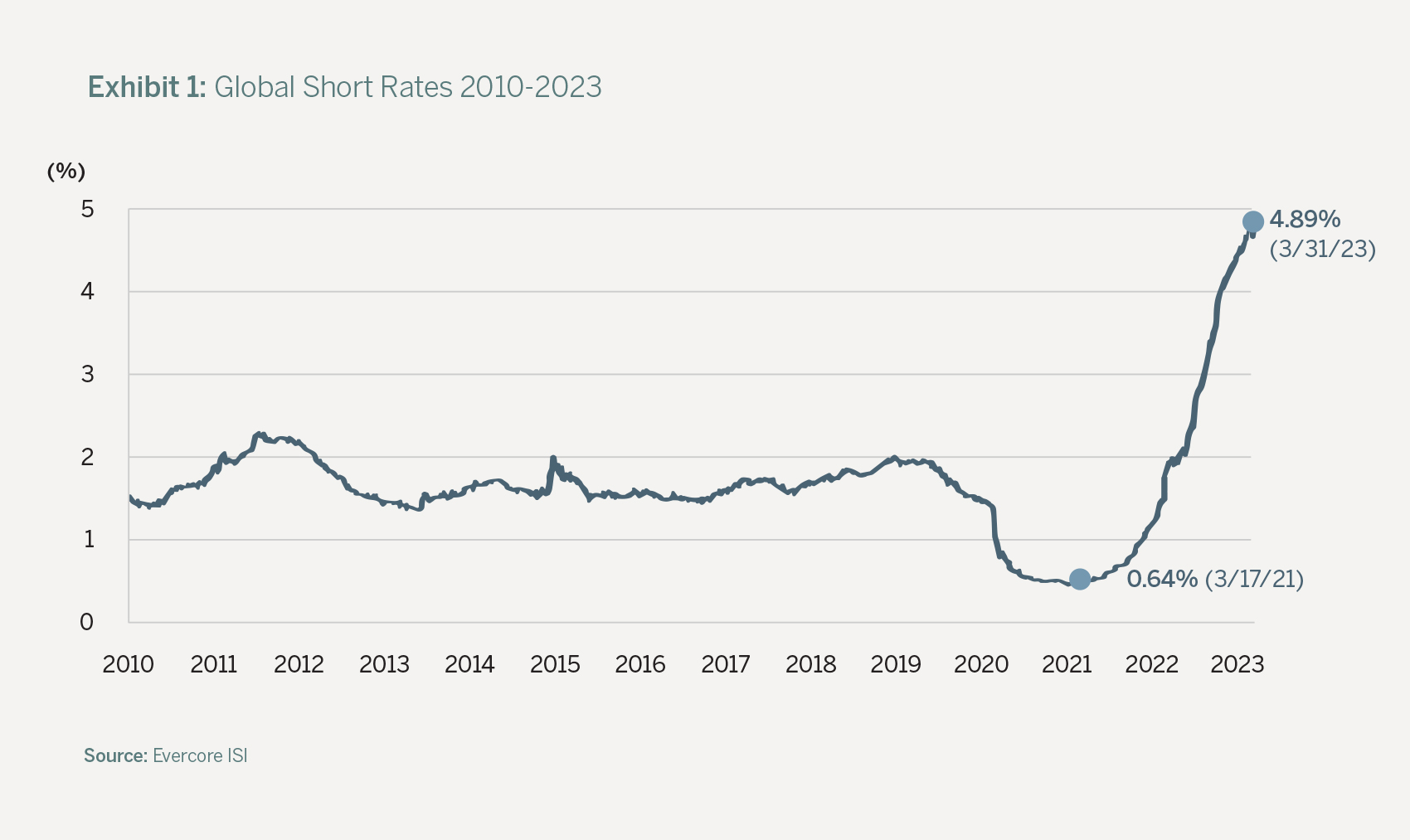

After a year of sharp interest rate hikes by central banks around the world (see Exhibit 1), investors entered 2023 expecting slower global and U.S. economic growth. Bullish investors hoped slower growth would bring down inflation, allowing central banks to end the rate hikes that have compressed earnings multiples and raised the cost of capital. Bearish investors believed that economic growth would fall to negative levels and significantly reduce corporate earnings before inflation declined. In January, it seemed as if the bulls were firmly in control. By early February, the S&P had risen almost 9%.

However, economic reports in late January and early February were surprisingly robust. Fears rose that central banks would hike rates more than expected to tame inflation, causing stock and bond markets to fall. By early March, the S&P 500 had given back almost all of its gains for the year.

Then word of Silicon Valley Bank (SVB)’s troubles led to rapid withdrawals by depositors in many U.S. regional banks. In a matter of days, SVB and Signature Bank (SBNY) were forced into receivership. Equity markets briefly sold off further, before rebounding as the U.S. government rushed to stabilize the banking system.

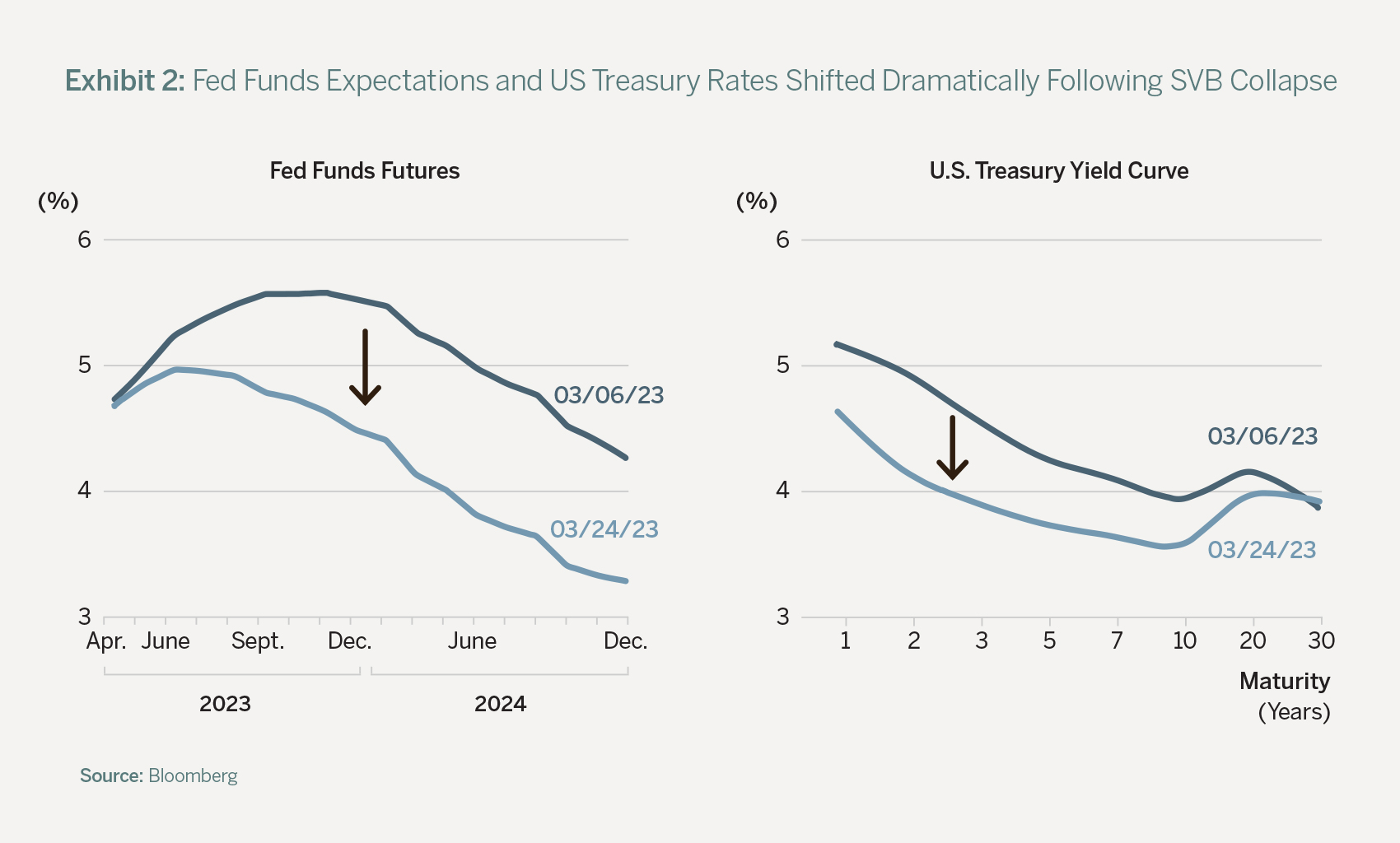

Investors quickly projected that banks would tighten lending standards so much that the Federal Reserve (Fed) would not need to raise the Fed Funds Rate as high as previously forecasted. Yields dropped across all maturities, but most notably for shorter-term debt (see Exhibit 2). Equity markets rose as the discount rate used to value future cash flows declined.

After this wild ride, the S&P 500 ended March at 4,109, delivering an impressive total return for the quarter of 7.5%. The bond market also had a strong quarter, as the Bloomberg Aggregate Bond Index posted a total return of 3.0%.

Behind the Regional Bank Turmoil

Much has been written about the causes of the largest bank failures in the U.S. since 2008. Both SVB and SBNY had specific company issues that made them particularly vulnerable to the rapid increase in interest rates that U.S. borrowers have been grappling with over the past year. But they certainly were not the only institutions experiencing withdrawals and losses on their bond portfolios.

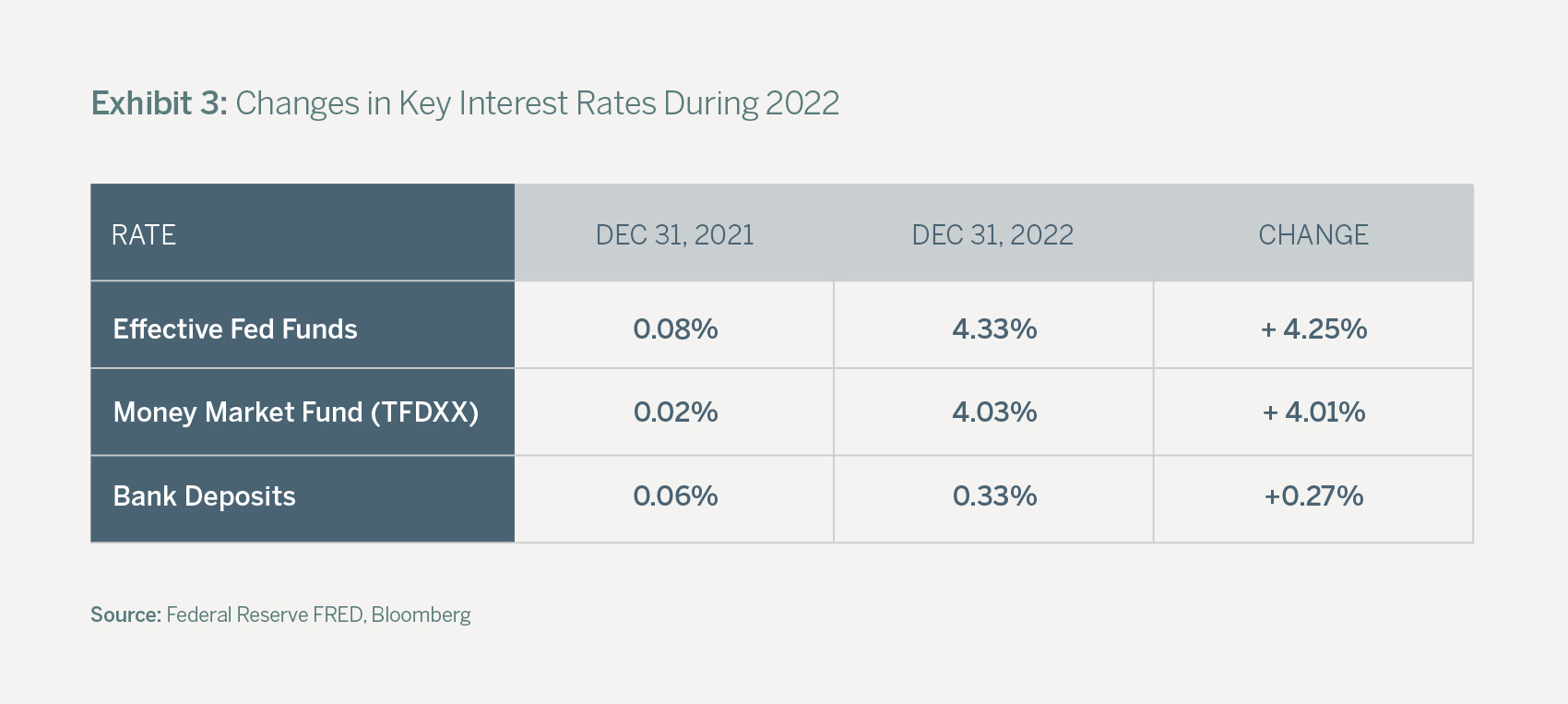

Widespread deposit withdrawals from U.S. banks began in 2022, but not from fear. While the Fed Funds rate rose, banks left deposit rates basically unchanged. As a result, depositors shifted their money from banks to higher-yielding money market funds and Treasuries. Aggregate U.S. bank deposits shrank in 2022 for the first year since 1948.

To fund withdrawal requests, banks were forced to sell fixed income holdings, causing them to book losses on their portfolios. In early March 2023, these pressures and the pace of deposit withdrawals led SVB and SBNY to become insolvent, and sparked fears of cascading bank failures. Regional bank stocks plunged.

If enough people fear that banks are unsafe, banks become unsafe. To stop the panic from leading to devastating runs on regional banks across the nation, U.S. officials took two actions. First, the FDIC guaranteed the deposits of all SVB and SBNY customers (including extremely large, uninsured depositors). Second, the Fed introduced the Bank Term Funding Program, which allows eligible depositories to borrow from the Fed against the full face value of their government bond portfolios. In one step, this effectively eliminated more than half a trillion dollars in unrealized losses that banks had incurred on these portfolios as the Fed raised interest rates.

Not Another GFC

For a few days, many investors feared a repeat of the Global Financial Crisis (GFC) of 2008-09, which plunged most of the world’s economies into deep recession and dragged down equity indices by as much as 50%. We see the circumstances today as very different.

In the GFC, very large financial institutions held massive quantities of complex mortgage-related securities that were illiquid and hard to value. In many cases, the underlying mortgages were also of very low quality. As banks tried to sell these securities, their prices plummeted, and the solvency of these institutions came into question.

In contrast, regional banks today mostly own U.S. Treasuries, mortgages, and government agency-backed securities that are easier to value and of higher quality. In addition, the prospect that bank weakness will reduce lending and slow the economy is leading to higher bond prices, thereby reducing bank losses. In that sense, today’s situation may be self-limiting, unlike the self-perpetuating nature of the GFC.

Further, money center banks and other very large financial institutions have been largely unaffected. After the GFC, these institutions were labeled “systemically important” and were subjected to higher capital requirements and closer regulatory oversight. As a result, they haven’t suffered from the same fear-based flight this year and have acted as a ballast for the banking system.

A “Goldilocks” Bank Crisis?

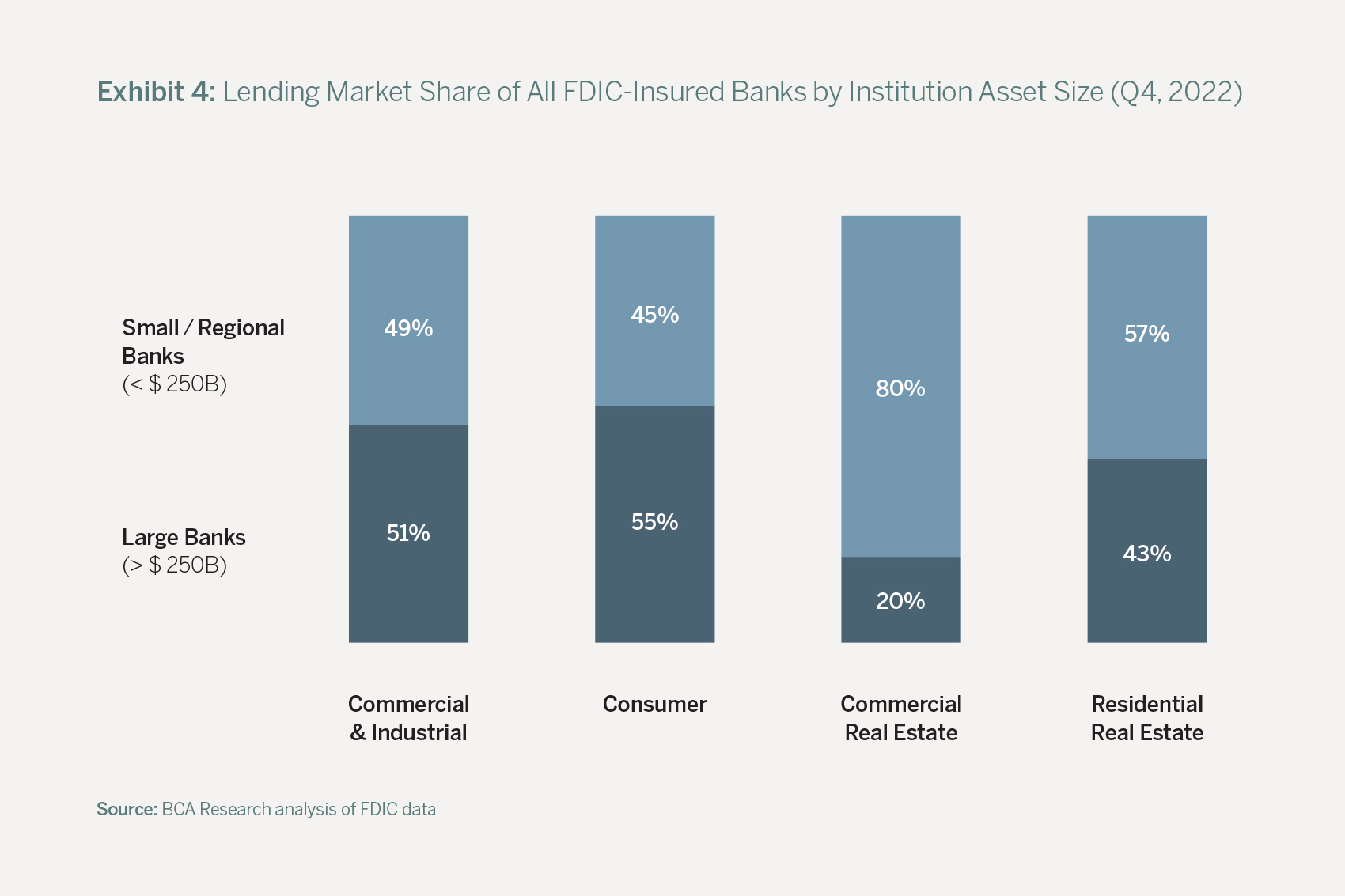

Bank crises almost always lead to economic slowdowns as banks pull back from extending credit. We expect the recent failures of a few regional banks and widespread deposit withdrawals to make most regional banks more cautious about lending. This has important implications for the economy. While individually small, regional banks as a group are an important engine of the economy. Collectively, they generate about half of all U.S. commercial and industrial (C&I) loans, and an even larger share of U.S. residential mortgage and commercial real estate loans.

But slower economic growth won’t necessarily be bad for equity markets. Counterintuitively, economic growth and financial market performance often move in opposite directions. Although strong growth may lead to higher corporate earnings, it also raises the specter of higher inflation and higher interest rates. When interest rates rise, investors apply a higher discount rate to future earnings and pay lower price-to-earnings (P/E) multiples for stocks.

More often than not, when interest rates rise, the negative impact on stock prices of falling P/E multiples outweighs the positive impact of higher earnings. That’s what happened in February. Stronger-than-expected economic growth raised fears of greater rate hikes, and stocks fell. In late March, by contrast, expectations of an economic slowdown or recession led to lower interest rates, and the stock market rallied.

Arguably, an economic slowdown that results from tighter credit would be better for equity markets than a slowdown that results from the Fed Funds rate approaching 6%. In both cases, corporate earnings are likely to decline, but in the higher interest rate scenario, a greater discount would likely be applied to future earnings, leading to lower equity prices.

How much will tighter lending standards slow economic growth? The U.S. economy has surprised most observers with its resilience and its insensitivity to rising rates. It now appears that equity investors are betting that these regional banking issues will be big enough to reduce or eliminate future rate increases, but small enough to avoid a deep recession. In other words, they are hoping that it will lead to an economy that, like Goldilocks’s porridge, is neither too hot nor too cold.

We think the odds that a recession will begin in 2023 are higher than they were three months ago. Companies in a wide swath of industries are likely to have a more difficult time raising capital and will be forced to tighten their belts. Layoff announcements are increasing. Unemployment will likely rise, and consumers may become more reluctant to spend.

But many economists and analysts have been calling for a recession for quite some time, and corporate earnings estimates have already fallen by 11% versus a year ago. Therefore, we don’t expect equity markets to sell off dramatically if a moderate recession ensues — unless inflation and interest rates remain stubbornly high.

Equity Portfolio Positioning

We are making several adjustments to Global Thematic Equity portfolios based on our expectations for lower U.S. economic growth or a mild recession.

First, we are decreasing the portfolio weight of our End of Disinflationary Tailwinds theme by reducing positions in a number of Energy sector companies within the theme. We expect that the sector may underperform near-term if recession fears grow. Longer-term, we remain bullish on Energy. We believe that the world will continue to rely on fossil fuels for many decades to come and that recent investment in the energy complex is inadequate to keep up with demand. The energy companies and servicers we follow stand to gain from this imbalance.

Second, we have increased the portfolio weight in our Next-Generation Automation theme. As the global labor force ages and Baby Boomers in the U.S. retire en masse, companies will have to find ways to do more with fewer people. We believe automation is the most cost-effective and productive way to address the labor shortage. We also believe automation has reached an exciting inflection point: The technologies needed are now available, and companies are now willing to make capital investments to acquire them. Our research has identified many automation-related opportunities. Most are companies that provide the advanced semiconductors that automation requires, industrial robots or inventory tracking systems. Because many of the opportunities we see are companies with headquarters outside the U.S. or that sell globally, increasing investments in this theme will also increase portfolios’ non-U.S. exposure.

Third, we are adding a bit to our Molecular Medicine theme and our Heterogeneous Computing theme, which increases portfolio exposure to Growth stocks. The stocks in these themes, like Growth stocks overall, came under pressure last year as interest rates rose. Many Growth stocks in these sectors rebounded nicely this year. We think their strong performance is likely to continue as the secular changes supporting these themes continue to unfold and as interest rates stabilize or decline.

Renewed Opportunities in Fixed Income

The low interest rates of the past decade created an unusual environment, in which many investors felt compelled to focus exclusively on equities to garner an adequate return. This mindset, dubbed TINA, for “There Is No Alternative,” is giving way. The significant rise in interest rates in 2022 has created an environment with greater opportunities in fixed income than we have seen in many years. In the space of a year, the market mindset has moved from TINA to TIA: “There Is an Alternative.”

As a result, we are working with many clients to review their overall asset-allocation strategies, and modifying the profile of the bonds we buy. We are optimizing target portfolio maturities, and seeking value from issuer selection and nimble execution. One area of focus has been the bonds issued by states with low or no state income tax.

Wealthy individuals have invested for decades in municipal bonds, particularly if they reside in states with higher income tax rates, because the interest on these bonds is generally exempt from state income tax for that state’s residents. We now see compelling opportunities for clients to invest in bonds issued by states with low or no state income taxes. These states often have less in-state demand because their residents are not subject to a state income tax. As a result, they may offer higher interest rates on their bonds to attract out-of-state demand. Today, rates on these bonds are high enough, even after accounting for taxes, to attract investors from high-tax states. These buyers may also benefit from the diversification of holding bonds from a larger number of states.

In Conclusion

The first quarter has been an eventful one, full of change, risks and opportunity. We remain committed to our investment philosophy and its pragmatic execution. We continue to monitor events carefully, and, as always, we will adjust our views and approach should developments suggest doing so.